Monthly Economic Review for December 2015

- Details

- Category: Economic Release

- Created: 25 February 2016

Global economic activity in 2015 remain subdued. In the US, economic activities remains strong, supported by accommodative financial conditions and improving housing and labor markets. However, growth momentum is expected to hold sturdy as dollar strength is expected to weigh on manufacturing activity. Despite falling commodity prices, a slowdown in China and a deterioration in international trade, the weak Australian dollar and low production costs have kept Australian iron ore producers competitive in global markets. New Zealand’s economy accelerated in Quarter 3, 2015 and grew at the fastest rate since Quarter 4, 2014. However, growth remains relatively weak in NZ as low commodity prices strained the key dairy industry and weighed on export growth. World oil prices continued to hover below US$45 per barrel during the month of December and recorded USD$36.59 per barrel at the end of month.

Overall domestic economic activity continue to support the NRBT’s forecast of stronger growth for 2015/16, supported by a growing construction sector, buoyant tourism industry, and a vibrant trade sector offsetting the seasonal decline in agricultural output during the month. A significant fall in total agricultural exports volume over the month by 81.5% reflects the end of the squash season. In addition, exports of cassava, taro tarua leaves, breadfruit and watermelon also declined over the month. This was largely due to adverse weather conditions.

Continued growth in air arrivals contributed to a $1.6 million and $11.0 million rise in travel receipts over the month and year to December respectively. The age group of 45 – 49 years of age has the highest number of visitors and it coincides with events taking place in December such as church conferences, school anniversaries, villages and various family re-unions.

The container registrations rose by 34.1% in December 2015 to its highest level on record and it may have contributed to the high government revenue collection during the month. Both private and business container registrations increased by 25.4% and 42.7% respectively, promoting growth in both the formal and informal parts of the distribution sector. Over the year ended December, container registrations also increased by 17.2%, with business container registrations increasing the fastest.

A significant increase in the total number of job advertisements1 over the month of more than 50 new vacancies was largely driven by an increase in job advertisements in the public administration sector particularly the Ministry of Education reflecting the preparation for the new academic year. In addition, job advertisements in the Private Sector also increased over the month. Over the year, job advertisements fell by 22.6% reflecting a strong government recruitment in early 2014.

Higher food prices pushed up the headline inflation over the month by 0.3%. Specifically, Domestic Food prices rose by 4.5% due to an increase in the prices of pawpaw, watermelon, dry coconut, peanuts, tomatoes, carrots, octopus, cockles (to’o) and also stringed fish (mixed). High demand for these domestic food items due to events taking place during the month could have contributed to the increase in prices. Imported prices however fell by 0.8% over the month as a result of lower prices for food items such as mutton flaps and chicken pieces while the decline in prices for petrol and diesel were reflected in the fall in Private Transportation prices.

In the year to December, headline inflation fell by 1.2%, in line with NRBT view that prices will remain subdued in 2015 and in the near term, mainly due to the slide in the price of crude oil. NRBT continues to expect that headline inflation will continue to remain low in the near term. However, risks to this forecast would be developments in world oil and food prices for both domestic and imported inflation.

The depreciation of the Tongan Pa’anga (TOP) against the New Zealand Dollar (NZD) and the Fijian Dollar (FJD) contributed to a decrease in the Nominal Effective Exchange Rate (NEER) of 1.0%, and the Real Effective Exchange Rate (REER) of 0.8%. In annual terms, both the NEER and REER declined as the TOP weakened against the USD, FJD and the AUD, maintaining Tonga’s price competitiveness against that of its major trading partners.

The Total Payments in Overseas Exchange Transactions (OET) for the month of December recorded a slight increase of 1.3% to $44.7 million. This was due to a $2.3 million increase in current account payments driven by an increase in import payments of $2.1 million, which were largely higher imports of wholesale and retail goods and construction materials supporting the vibrant domestic economic activities. Capital account payments, on the other hand, fell by $1.9 million due to a fall in private capital transfers.

Total OET Receipts increased in December by 45.1% to $59.5 million, the highest level recorded for 2015. Receipts from the current account rose by $10.2 million, followed by the financial account with $6.0 million and the capital account by $2.3 million. The higher financial account receipts were mainly due to increasing funds transfers by resident businesses and non-profit organisations from their deposits in non-resident banks during the month.

The balance of OET for the month of December recorded a surplus of $8.8 million, $5.7 million higher than that in the previous month, contributing to the higher level of foreign reserves. Gross foreign reserves has consistently remained above the $300 million mark in the past 5 months, reaching another new record high of $327.8 million at the end of December. This is equivalent to 9.6 months of import cover, well above the NRBT’s minimum range of 3-4 months.

Broad money increased to a new record high of $450.2 million in December. This was driven by a 7.3% increase in net foreign assets and 0.2% rise in net domestic assets. The growth in net foreign assets resulted from a rise in foreign reserves whilst an increase in lending drove the higher net domestic assets. However, banking system liquidity fell slightly over the month by 1.0% to $169.4 million, reflecting increases in banks withdrawing their deposits with NRBT to facilitate spending during festive season. This coincides with a rise in currency in circulation over the month.

Total bank lending slightly rose over the month by 0.5% to $325.4 million. Household loans drove the increase whilst business and other loans fell by 1.3% and 2.5% respectively. The settlement of business loans suggests buoyant business conditions enhancing businesses’ repayment capability and coincides with the higher government revenue collection, indicating stronger domestic economic activity. The increase in household loans, however, were underpinned by continued growth in housing loans and coincides with the continued lower housing lending interest rates. Including loans extended by non-banks, total lending increased by 0.4%, underpinned by growth in household loans.

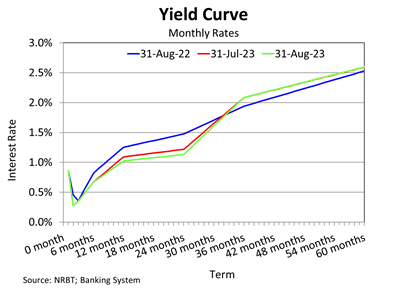

Weighted average interest rate spread widened over the month from 5.89% in November to 5.92% in December 2015. This resulted from a 2.5 basis points fall in weighted average deposit rate to 2.15% which outweighed a 0.2 basis points decline in the weighted average lending rate to 8.07%. Increased competition amongst banks has driven the lower weighted average lending rate underpinned mainly by declines in businesses and other personal lending rates whilst the increase in deposits caused the decline in weighted average deposit rate.

Net credit to government fell by 2.9% due to a 2.2% rise in government deposits reflected a strong fiscal position at the end of December. This reflects higher government revenue collection during the month, including the receipt of dividends from Tonga Airports Ltd of $1.3 million and Tonga Asset Managers and Associates Ltd of $0.05 million. This also coincides with the record number of container registrations in December, which is in line with the festive events during the month. In year ended terms, net credit to government rose by 13.3% driven by a 10.1% decline in government deposits due to delays in receiving funds from donor partners.

Domestic economic activities remained broadly positive during the month of December. Tonga continue to benefit from global developments. Inflation remains relatively low largely supported by the low global oil prices. Monetary conditions improved as total credit and deposits continued to grow, and narrow weighted average interest rate spreads remains. Tonga’s financial system remains sound as the banking system continued to be profitable with strong liquidity and capital position being maintained. Consistent with the high banking system liquidity, broad money increased to its highest level and foreign reserves remained well above the minimum range. Given the above developments, the current monetary policy stance remain appropriate in the near term.

The NRBT will continue to promote prudent lending, closely monitor credit growth and be mindful of the impact of a continued deflation. The NRBT will closely monitor the country’s economic developments and financial conditions to maintain internal and external monetary stability, promote financial stability and a sound and efficient financial system to support macroeconomic stability and economic growth.

Download the full review here.

1 - This is based on job advertisements published on local newspapers (Taimi, Talaki and Kele’a) and the Matangi Tonga Website).