Monthly Economic Review for May 2015

- Details

- Category: Economic Releases

- Created: 24 July 2015

Global developments continue to be supportive of domestic economic growth. Unemployement rate in Australia dropped to a one year low of 6.0% from 6.1%. New Zealand’s unemployment rate remained stable while the US unemployment rate was up from 5.4% to 5.5% due to more people joining the workforce. Both the New Zealand dollar and the Australian dollar fell against the stronger U.S. dollar making imports cheaper from those countries.

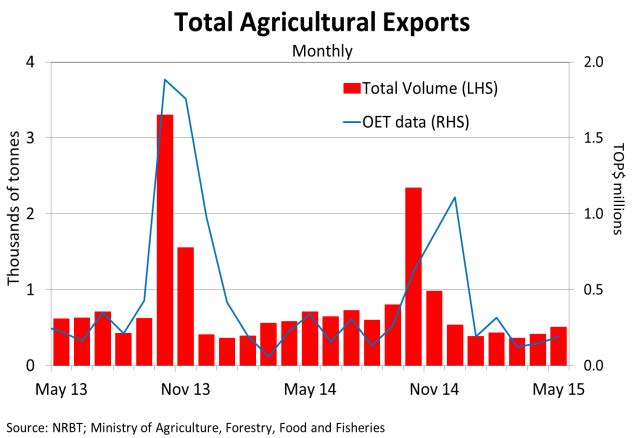

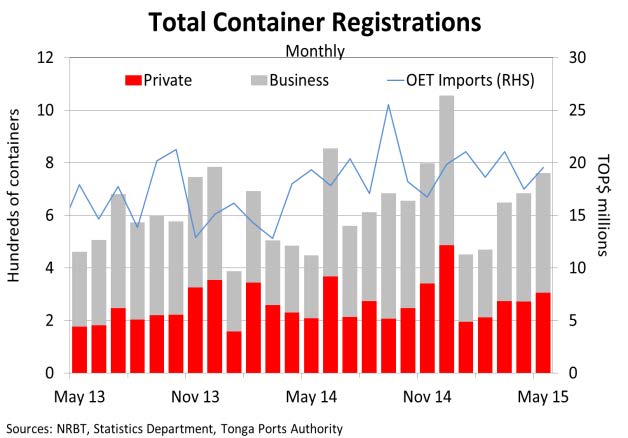

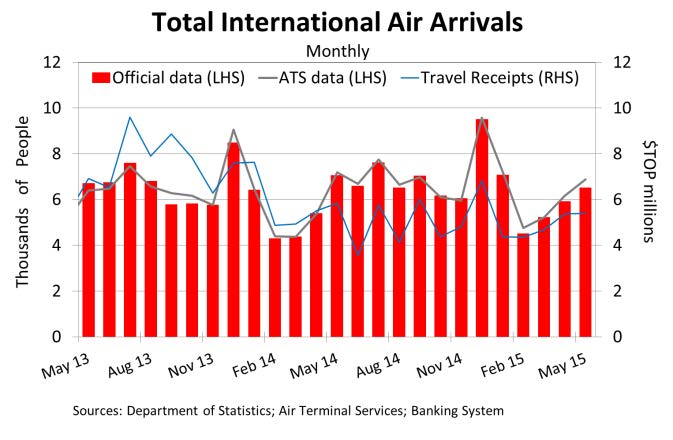

The domestic economy expanded over the month of May. Favourable weather conditions in recent months helped the agricultural sector improve. Agricultural exports volume increased by 23.2% due to increases in exports of root crops. Proceeds from agricultural and marine exports increased by 30.5% and 34.6% respectively, both signifying a lively primary sector. The retail and wholesale sector improved, in line with an 11.1% increase in container registrations. Payments for imports excluding oil also showed an increase over the month. Visitor air arrivals also increased by 9.5% indicating an active tourism sector. Travel receipts through the banking system also showed an increase. The strengthening tourism sector is expected to also benefit the transportation sector, especially tour operators. Vehicle registrations over the month were relatively stable.

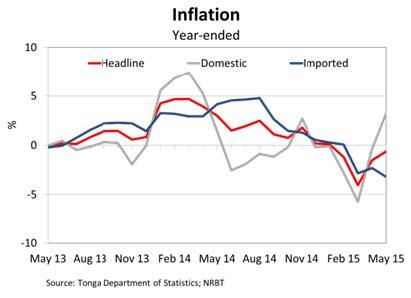

CPI fell by 0.1% over the month due to a decline in Imported prices, particularly Food items such as Fruit & vegetables, and Meats, fish & poultry. The Tongan Pa’anga appreciated against the New Zealand Dollar which could have contributed to the lower imported food prices. Contrastingly, prices for Domestic fuel and power, and Transportation increased over the month due to recovering global oil prices. This led to Domestic prices rising by 0.4%, slightly offsetting the monthly deflation.

Over the year, the headline inflation rate decreased by 0.6% due to global energy prices being 29% lower than the previous year. Consequently, this drove Imported prices down by 3.2%, specifically for the Household Operation and Transportation components. Furthermore, Imported Food prices dropped by 2.1% as a result of lower prices for Meats, fish & poultry, and Cereals & cereal products. On the contrary, Domestic prices increased by 3.2% due to higher Domestic Food prices, particularly local Fruit & vegetables.

Over the month of May, the Pa'anga stregthened against the New Zealand dollar and Australian dollar, whilst falling against the US dollar. The Nominal Effective Exchange Rate (NEER) changed little from last month while the Real Effective Exchange Rate (REER) index fell slightly, indicating an improvement in Tonga’s competitiveness against its major trading partners. In year-ended terms both the NEER and REER fell by 1.0% and 3.0% respectively.

Import payments, which make up a significant portion of the Current account, rose by around 44% over May. This was due mainly to a rise in payments made for oil imports. Total Export receipts were 15% more than last month, with proceeds from fish and other marines rising faster than that of Agricultural exports. Remittances, on the other hand, rose significantly by 80% to $28.6 million. This comes as no surprise with the celebrations of Children’s Sunday, Mothers Day and Fathers Day held in May. Remittances is anticipated to be around the same levels next month in the lead up to the coronation.

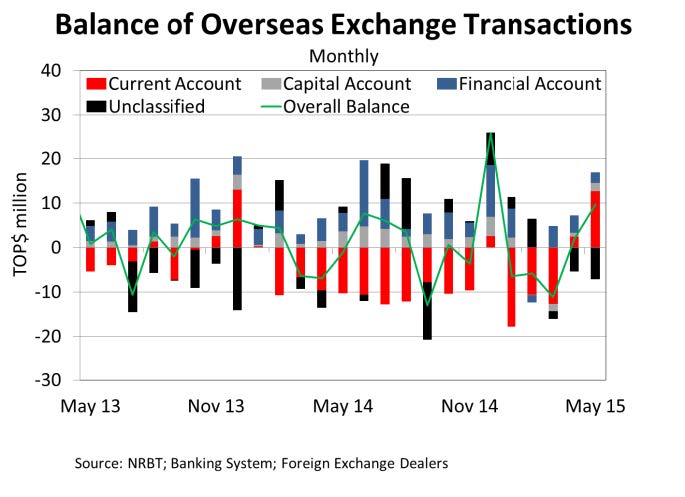

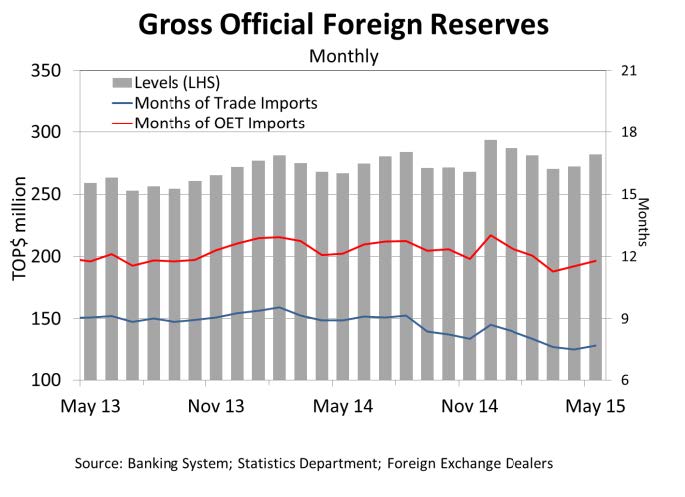

The balance of Overseas Exchange Transactions over the month of May was a surplus of $9.7 million, much higher than the surplus of $1.8 million in April. This stemmed from a significant rise in remittances and official transfers. As a result, foreign reserves rose by $9.7 million over the month of May to $281.8 million, sufficient to cover 7.7 months of imports, well above the NRBT’s minimum range.

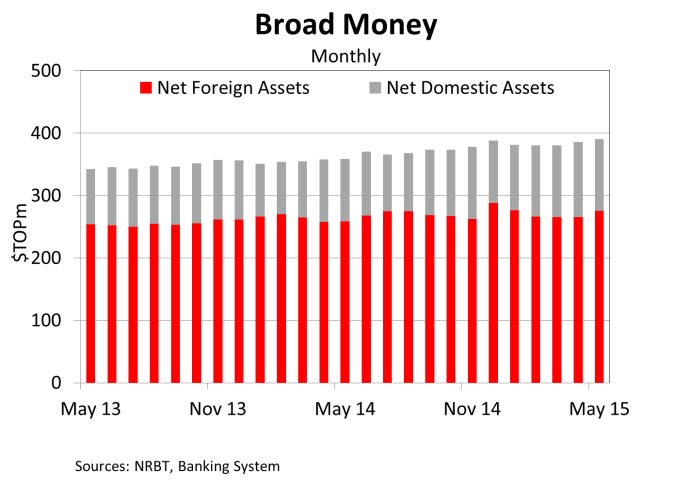

Broad Money increased over May by 1.2% due to a 3.8% rise in net foreign assets more than offsetting a 4.5% decline in net domestic assets. The increase in net foreign assests was driven by a rise in foreign reserves while net domestic assets fell due mainly to an increase in government’s deposits. Total domestic demand deposits and currency in circulation also increased in line with the rise in broad money. However, banking system liquidity fell slightly over the month by 0.8% due to a slight decline in deposits.

Total lending increased slightly over May by 0.9%, driven mainly by a 1.1% rise in household loans. The increase in household loans was largely attributed to a rise in other personal loans, which was supported by lending actitivities through the non-banking systems. Business lending also increased over the month, resulting mainly from a rise in banks’ lending to non-bank financial businesses. Additionally, more than 60 new loans were approved from the Government’s managed funds loan scheme during the month, which totaled to more than $1 million. Over the year, total bank lending rose by 7.7% driven mainly by a 15.1% increase in household lending. The increase in loans indicates growing economic activities in the Kingdom, underpinned by local festivities.

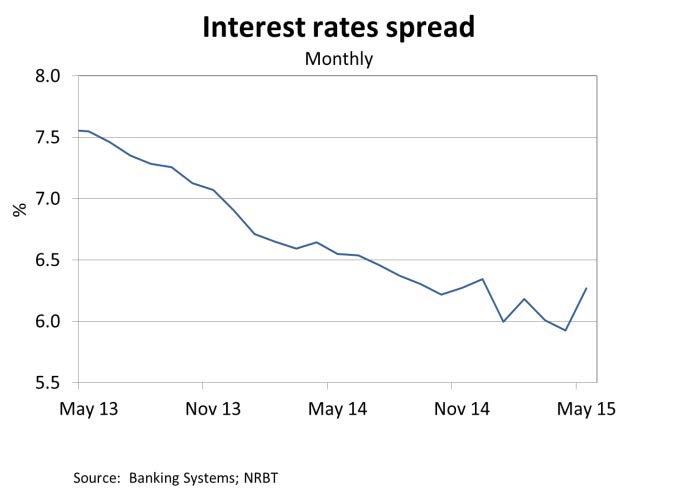

Weighted average interest rate spread widened over the month from 5.92% to 6.27%, reflecting a 5.3 basis points increase in weighted lending rate to 8.32%, and a 2.7 basis points rise in weighted deposit rate. The increase in weighted lending rates was driven by a hike in interest rate for business loans, whilst increases in savings and term deposit rates drove the rise in weighted average deposit rates.

Net credit to government fell for the first time in 2015 by about 17% due to around 12% increase in government deposits over the month. The receipt of Budget Support during the month contribute to the rise.

The outlook for domestic economic activities remains positive. Inflation is expected to remain low reflecting weak global commodity prices. The lower prices in turn is expected to support economic activities. Foreign reserves will continue to be montiored and kept above the NRBT’s minimum range of 3-4 months of imports. The banking system continued to remain relatively stable and profitable, with reported credit growth and strong liquidity and capital positions. The existing monetary policy setting is therefore considered appropriate in the near term.

The NRBT will continue to promote prudent lending, closely monitor credit growth and be mindful of the impact of a continued deflation. The NRBT will closely monitor the country’s economic developments and financial conditions to maintain internal and external monetary stability, promote financial stability and a sound and efficient financial system to support macroeconomic stability and economic growth.

|

|

|

|

|

|

|

|

Download the latest Monthly Economic Review to find out more.