Monthly Economic Review for June 2015

- Details

- Category: Economic Releases

- Created: 14 August 2015

Developments among Tonga’s key trading partners were mixed yet continue to support domestic activity. Unemployment in the US remained unchanged at 5.3% while it climbed in New Zealand and Australia to 5.9% and to 6.1% respectively. World oil prices continued to fall over the month of June and over the year by more than 40% to $62USD per barrel.

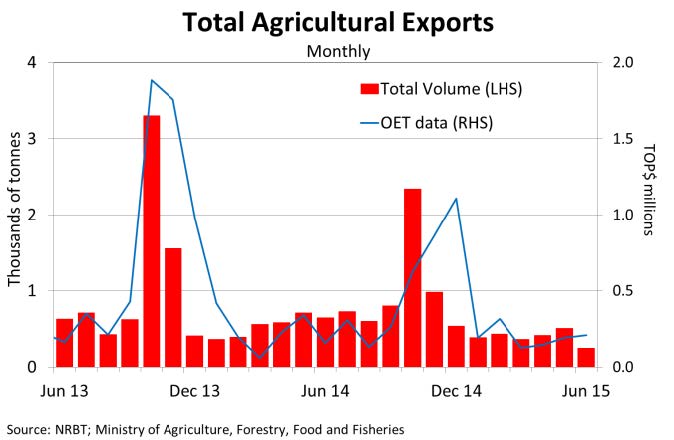

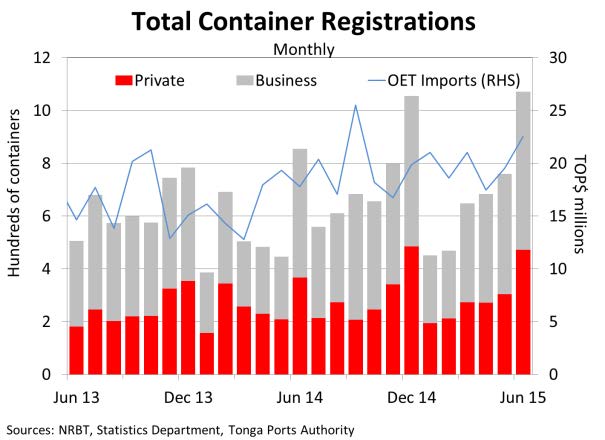

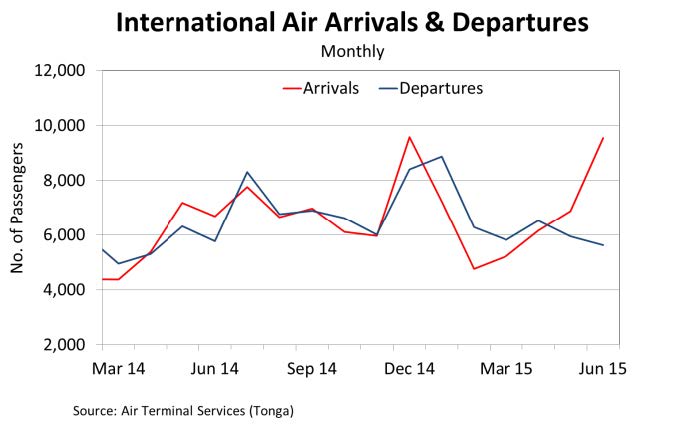

Despite a contraction in the primary sector, all other sectors advanced which boosted the domestic economy over June. This is linked to preparations for the coronation in July. Agricultural exports volume fell by 50.9% due to declines in root and vegetable products. However, proceeds from agricultural exports increased by 9.6% whereas fisheries exports decreased by 59.1%. This could be due to a lag effect in payments for exports. The trade sector advanced, coinciding with a 41.1% rise in container registrations (1,072 containers) being the highest number on record yet. Payments for imports excluding oil also showed an increase over the month. International air arrivals also increased by 38.9% indicating an active tourism sector. Travel receipts through the banking system supported the influx of arrivals and rose by 29.3%. The strengthening tourism sector is expected to also benefit the transportation sector, especially tour operators. Vehicle registrations rose by 33.7% caused by an influx of donor-funded vehicles for the coronation.

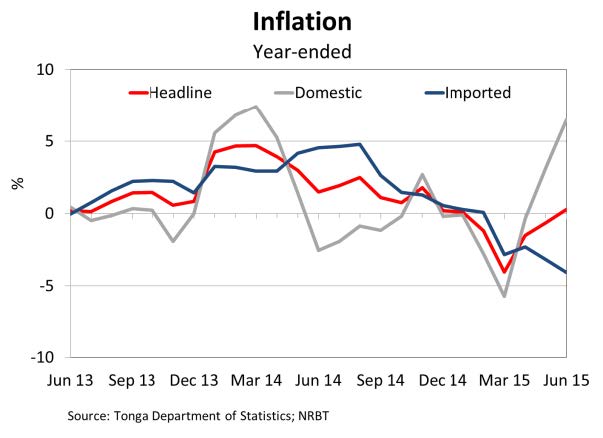

The monthly CPI decreased by 0.7% as a result of lower Imported and Domestic prices. In particular, lower Food prices drove imported inflation down. The Tongan Pa’anga appreciated against the New Zealand Dollar which could have contributed to the low imported food prices. Additionally, the fall in Domestic inflation was caused by a decrease in prices for Household Supplies & Services.

After four consecutive months of headline deflation, the inflation rate was 0.2% over the year to June. This was caused by Domestic prices which increased by 6.6%, offsetting a 4.1% decline in Imported prices. Prices for food items, namely Fruit & Vegetables and Meats, Fish & Poultry caused a 21.5% increase in Domestic Food prices whereas the same food items drove Imported Food prices down by 4.3%. Contrastingly, Domestic Fuel & Power prices fell over the year affecting the Household Operation and Transportation components. However, this was insufficient to offset the rise in Food prices.

Over the month of June, the Pa'anga strengthened against the New Zealand dollar, whilst falling against the Australian and US dollar. The Nominal Effective Exchange Rate (NEER) changed little from last month while the Real Effective Exchange Rate (REER) index fell by around 1%, indicating an improvement in Tonga’s competitiveness against its major trading partners. In year-ended terms both the NEER and REER fell by around 1.0%.

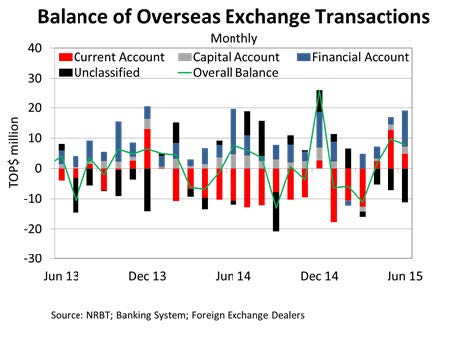

Import payments remained at high levels of $26.6 million over June. Driving the rise were mainly payments for wholesale & retail goods and construction materials. Total Export receipts were 8% more than last month, with proceeds from agricultural products like vanilla, coconuts and kava rising faster than fish and other marine exports. Additionally, travel receipts contributed to the rise. Remittances1 were at high levels of around $24.7 million, slightly lower than last month, yet still remains the second highest recorded level of the past year.

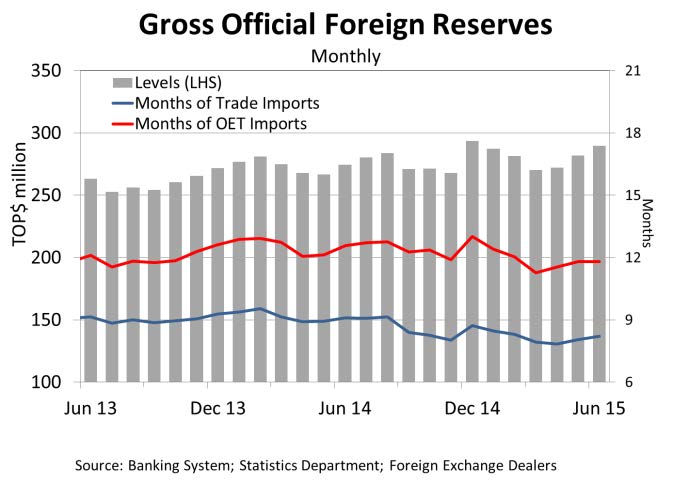

The balance of Overseas Exchange Transactions over the month of June was a surplus of $7.8 million though less than the surplus in May. The lower surplus in June stemmed from a lower current account balance. This was due to an increase in import payments more than offseting the increase in export and travel receipts, combined with the slight decrease in remittance receipts. As a result, foreign reserves rose by $7.9 million over the month of June to $289.7 million, sufficient to cover 8.2 months of imports, well above the NRBT’s minimum range.

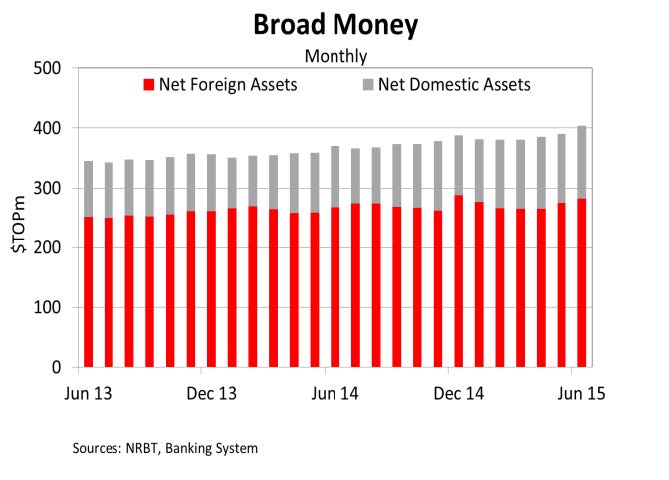

Broad Money increased over June by 3.5% due to a 5.4% rise in net domestic assets and a 2.7% rise in net foreign assets. The rise in net domestic assets reflects the increase in lending while an increase in foreign reserves drove the increase in net domestic assets. Broad money also increased over the year by 9.3%, underpinned by the increases in net domestic assets and net foreign assets.Total domestic demand deposits and currency in circulation also increased in line with the rise in broad money. Banking system liquidity rose over the month by 7.6%, resulted from the higher deposits and the increase in foreign reserves. Over the year, banking system liquidity increased by 13.7% respectively, due to the increases in deposits and foreign reserves.

Total lending increased slightly over June by 0.7%, driven mainly by a 1% rise in business loans. The increase in business loans was mainly driven by a rise in lending to the manufacturing and construction sectors from the Government’s managed funds loan schemes. A drawdown to public enterprises also supported the increase in business lending. Household lending also increased slightly over the month by 0.3%, driven by a rise in other personal lending. Additionally, about more than 30 new loans were approved from the managed funds during the month, totaled to more than $0.5million. In year ended terms, total bank lending rose by 7.8% driven mainly by a 13.7% increase in household lending. The sustained increase in lending indicates strong economic activities in the Kingdom, underpinned by preparations for the coronation, school reunions and the Free Wesleyan Church’s annual conference.

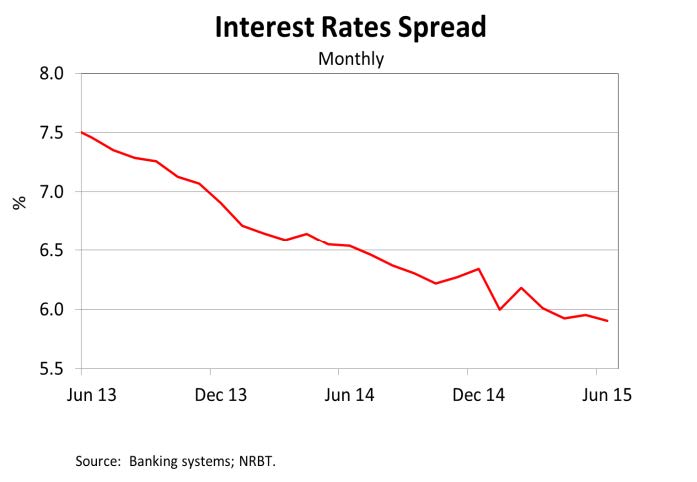

Weighted average interest rate spread widened over the month from 5.92% to 6.27%, reflecting a 5.3 basis points increase in weighted lending rate to 8.32%, and a 2.7 basis points rise in weighted deposit rate. The increase in weighted lending rates was driven by a hike in interest rate for business loans, whilst increases in savings and term deposit rates drove the rise in weighted average deposit rates.

Net credit to government rose by about 7% over June. The turnaround was due to a 5% fall in government deposits over the month as government clears its commitments and payments obligations before the end of the financial year. Over the year to June, net credit to government also increased by more than 8% underpinned by more than 15% rise in banks’ bond holdings due to new bond issue during the financial year and a 2% fall in government deposits.

The outlook for domestic economic activities remain positive. Inflation is expected to remain low reflecting weak global commodity prices. The lower prices in turn is expected to support economic activities. Foreign reserves will continue to be monitored and kept above the NRBT’s minimum range of 3-4 months of imports. The banking system continued to remain relatively stable and profitable, with reported credit growth and strong liquidity and capital positions. The existing monetary policy setting is therefore considered appropriate in the near term.

The NRBT will continue to promote prudent lending, closely monitor credit growth and be mindful of the impact of a continued deflation. The NRBT will closely monitor the country’s economic developments and financial conditions to maintain internal and external monetary stability, promote financial stability and a sound and efficient financial system to support macroeconomic stability and economic growth.

1 - As of May 2015 due to changes in methodology, Remittances is now defined as the sum of personal transfers, private capital receipts, social benefits and salary and wages. For further information, please refer to the Remittances report now available on the NRBT website.

|

|

|

|

|

|

|

|

Download the latest Monthly Economic Review to find out more.