Monthly Economic Review for July 2015

- Details

- Category: Economic Releases

- Created: 22 September 2015

Developments among Tonga’s key trading partners varied yet continued to support domestic activity. Unemployment in the United States and New Zealand remained unchanged at 5.3% and 5.9% respectively, while it climbed in Australia to 6.3% from 6.1%. World oil prices fell over the month of July by 13.9% to US$53 per barrel. The Tongan Pa’anga appreciated against the New Zealand and the Australian dollar which may exert some pressure on Tonga’s export industries and other receipts such as travel and remittances, while easing imported inflation.

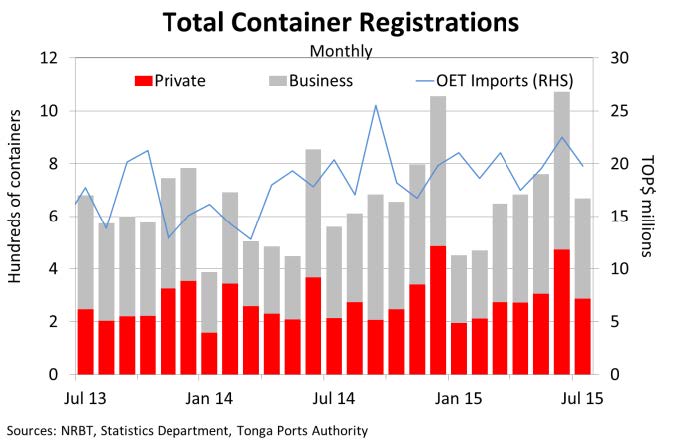

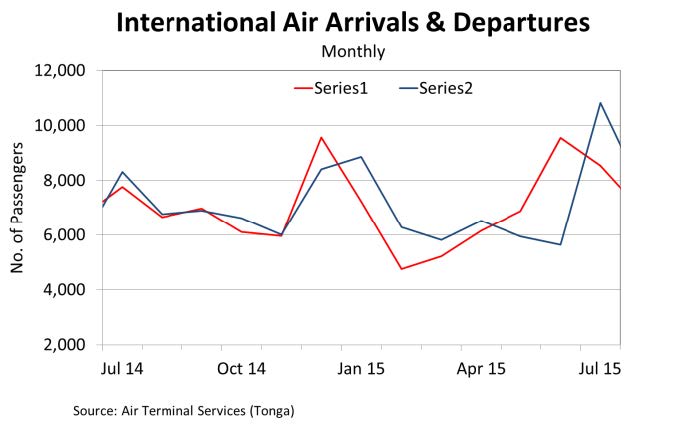

The domestic economy slowed down over July possibly due to the end of coronation celebrations and festivities. International air arrivals dropped by 10.6% whilst international departures almost doubled as visitors left Tonga, marking the end of the events over the month. A resulting slow down in activities in the tourism sector is expected. The 8.4% drop in vehicle registrations may be linked to the fall in tourism arrivals as well as a decline in vehicle loans over the month. The trade sector also eased, coinciding with a 37.6% fall in container registrations. Additionally, payments for imports excluding oil decreased over the month.

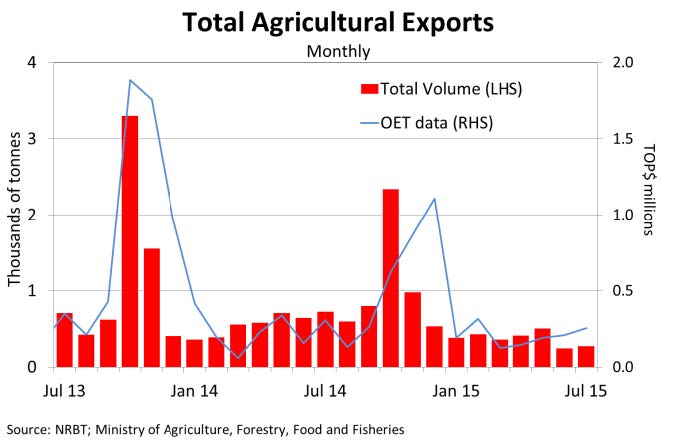

On the other hand, agricultural exports volume rebounded and rose by 9.6% in July. This was caused by more root vegetable products and other vegetable products. Proceeds from agricultural exports increased over the month, further supporting the monthly rise.

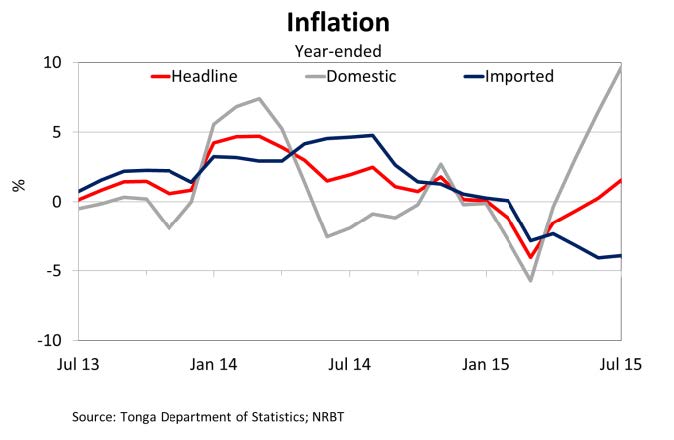

CPI rose by 1.3% over July as a result of Domestic and Imported prices increasing by 2.6% and 0.3% respectively. Specifically, Domestic Food prices for Fruit & Vegetables, and Meats, Fish & Poultry rose due to recent unfavourable weather conditions affecting supply. With the appreciation of the Tongan Pa’anga against the New Zealand Dollar and price of food overseas falling, Imported Food prices should have dropped, holding all things equal. However, the lag effect of recovering global prices exerting pressure on transportation costs and the appreciation of the US Dollar, more than offset this fall in prices, causing an overall rise in the price of Imported Food.

In annual terms, the headline inflation rate rose by 1.6% due to a 9.7% increase in Domestic prices. This was caused largely by higher prices for local food items such as Fruit & Vegetables, and Meats, Fish & Poultry which had also offset declines in prices of other Domestic items. In contrast, Imported prices dropped by 3.9% over the year as a result of lower Food prices for most food items. Additionally, the 49.7% decline in global oil prices greatly lowered the Transportation costs and the Household Operations component, specifically electricity prices.

The Nominal Effective Exchange Rate (NEER) changed little from last month while the Real Effective Exchange Rate (REER) rose by around 1%, indicating local commodities were more expensive against our trading partners due to higher domestic inflation. In year-ended terms both the NEER and REER fell by around 1.0% .

Import payments over July stood at $21.3million, slightly lower than the past two months. The higher imports in the two preceding months may have been in preperation for the coronation, held in the first week of July. With the end of these celebrations, imports for wholesale, retail goods and other goods dropped over July. Total Export receipts were 30% less than last month, driven by lower proceeds for marine exports. This is despite proceeds from agricultural exports being relatively high, in line with the rise in agricultural export volumes. Travel receipts rose over the month by 35% to $9.3 million. Although air arrivals decreased, departures increased and may explain the rise in travel receipts, as visitors pay for accommodation, gifts, souvenirs and other spending prior to departing. Lastly, Remittances remained high at approximately $21.8 million, around 14% more than in June and the highest recorded for this year.

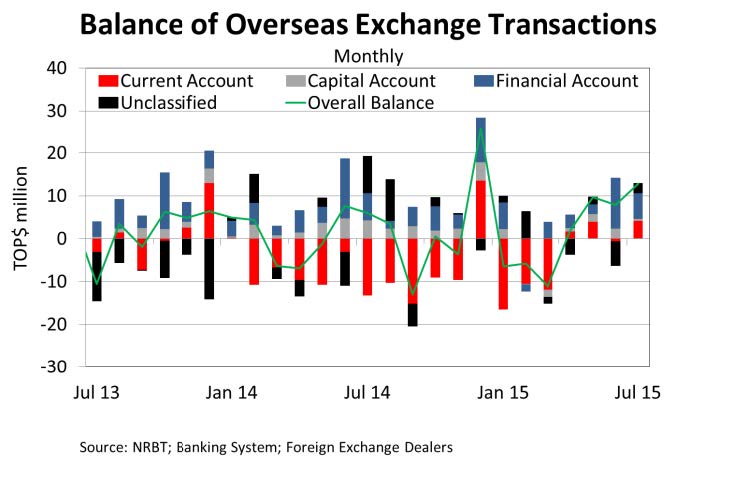

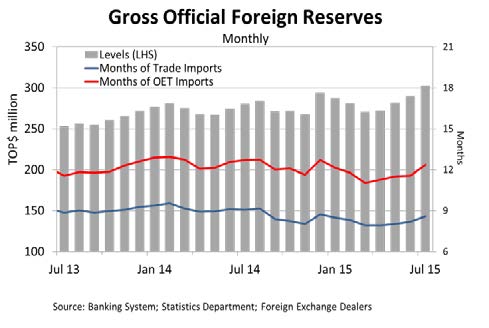

The balance of Overseas Exchange Transactions over the month of July was a surplus of $12.9 million, much higher than the surplus in June. The outcome stemmed from a higher current account balance. This was due to less net outflows in the trade balance combined with private transfer receipts more than offsetting a rise in official transfer payments. As a result, foreign reserves rose by $12.9 million over the month of July to $302.6 million, sufficient to cover 8.6 months of imports, well above the NRBT’s minimum range.

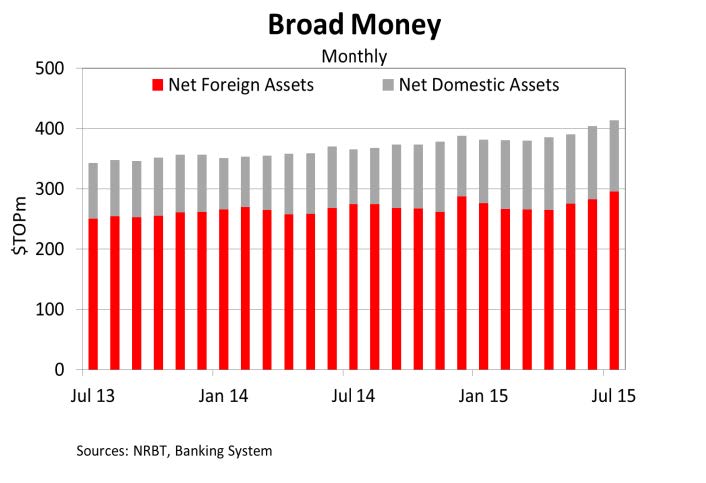

Broad Money increased over June by 2.9% due to a 4.2% rise in net foreign assets, offsetting a 1.9% decline in net domestic assets. The increase in net foreign assets reflects the increase in foreign reserves while a 3.8% decline in capital accounts driven mainly by a decline in banks’s retained earnings drove the lower net domestic assets. Broad money also increased over the year by 13.4%, underpinned by increases in net domestic assets and net foreign assets. Total domestic demand deposits and currency in circulation also increased in line with the rise in broad money. Banking system liquidity rose over the month by 5.9%, which resulted from the higher deposits and the increase in foreign reserves. Over the year, banking system liquidity increased by 17.8%, due to increases in deposits and the foreign reserves.

Bank lending increased slightly over the month by 0.5% due to increased lending to households. Including loans extended by non- banks, total lending rose by 0.2%. About more than 50 new loans were approved from the Government’s managed funds loan scheme during the month, totalling more than $0.6million. Over the year, total bank lending increased by 11.7% driven by a 13.7% and a 11.0% increase in business and household lending respectively. Including loans extended by non-banks, total lending rose by 8.0%, reflecting lower on-lent loans by the government.

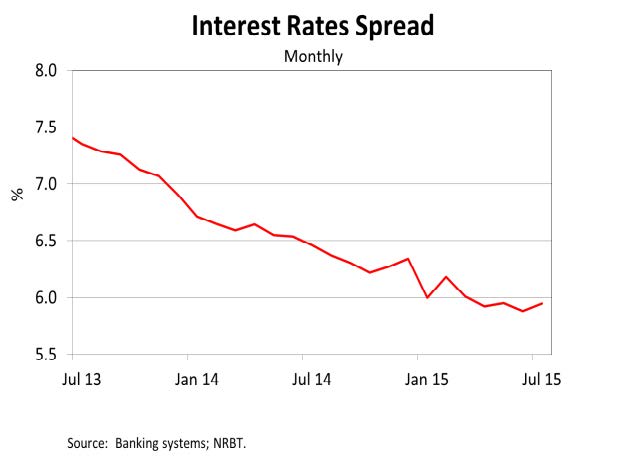

Weighted interest rate spread widened over the month from 5.88% to 5.95% in July 2015. This was due to a 0.3 basis points increase in weighted average lending rate to 8.23%, and a 6.4 basis points drop in weighted average deposit rate.

Net credit to government slightly declined in July 2015, therefore, adds to the fall in net domestic assets. This follows a slight increase in government deposits. Contributing to the rise in broad money over the year, net credit to government rose by about 13% due mainly to a decline in government deposits more than offsetting a decline in bonds held by banks.

Developments in the major trading partners’ economies, particularly the lower commodity prices, supports the positive NRBT outlook for Tonga’s economy. Early signs of improvement are evident from the agricultural sector. We also expect robust credit growth as business confidence and conditions improve. The banking system continued to remain relatively stable and profitable, with reported credit growth and strong liquidity and capital positions. Although the New Zealand dollar depreciated, it had little impact on remittances and travel receipts from New Zealand, both of which increased over the month of July. On the other hand, businesses and other consumers enjoyed lower import prices in line with the exchange rate weaken. Low inflationary and liquidity pressures together with ample foreign reserves provide no requirement to adjust monetary policy settings in the near‐term.

The NRBT will continue to promote prudent lending, closely monitor credit growth and be mindful of the impact of a continued deflation. The NRBT will closely monitor the country’s economic developments and financial conditions to maintain internal and external monetary stability, promote financial stability and a sound and efficient financial system to support macroeconomic stability and economic growth.

|

|

|

|

|

|

|

|