- Monthly Economic Update - April 2026 DOWNLOAD THE FULL UPDATE | PDF • 605 KB

Outlook

This monthly update reports on February 2026 data. However, the Middle East conflict, which escalated quickly since end of February 2026, has taken centre stage in all economic outlooks. By April, its impacts have reached Tonga, through

significant rises in fuel prices of more than 20% for petrol and more than 40% for diesel. Authorities are stepping up policy decisions to ensure that adequate supplies are maintained and the public remains calm despite the inevitable oil supply shock that is happening worldwide.The outlook for inflation is expected to remain above the NRBT’s 5% reference rate, with the fluctuation dependant on the impact and duration of the conflict. Rising global oil prices are expected to push up costs for goods and services, and these pressures could persist if oil prices stay elevated, even during recovery. With limited domestic production capacity to absorb external shocks, there is a higher risk of cost passthrough and sustained inflationary pressure. Official foreign reserves are expected to remain above minimum thresholds in the near term supported by external inflows. However, the medium-term outlook remains uncertain and is tilted to the downside, particularly if the ongoing Middle East crisis intensifies. The financial system remains stable, supported by strong capital buffers and adequate liquidity. However, credit growth is expected to be constrained due to the condition of existing loan portfolios. Non-performing loans (NPLs) may rise further if the Middle East crisis intensifies, as businesses and households could face greater difficulty servicing debt, leading to higher default rates. Maintaining asset quality will therefore be essential to safeguard macroeconomic stability and support future growth. Given these developments and outlook, the NRBT and the Government continue close coordination to mitigate inflation risks from the crisis. The NRBT notes will remain in use to manage excess liquidity and strengthen monetary policy transmission to market interest rates. Ongoing efforts also focus on improving liquidity management, reactivating the interbank market, modernising payment systems, and deepening financial markets.

Global economy facing war-driven headwinds

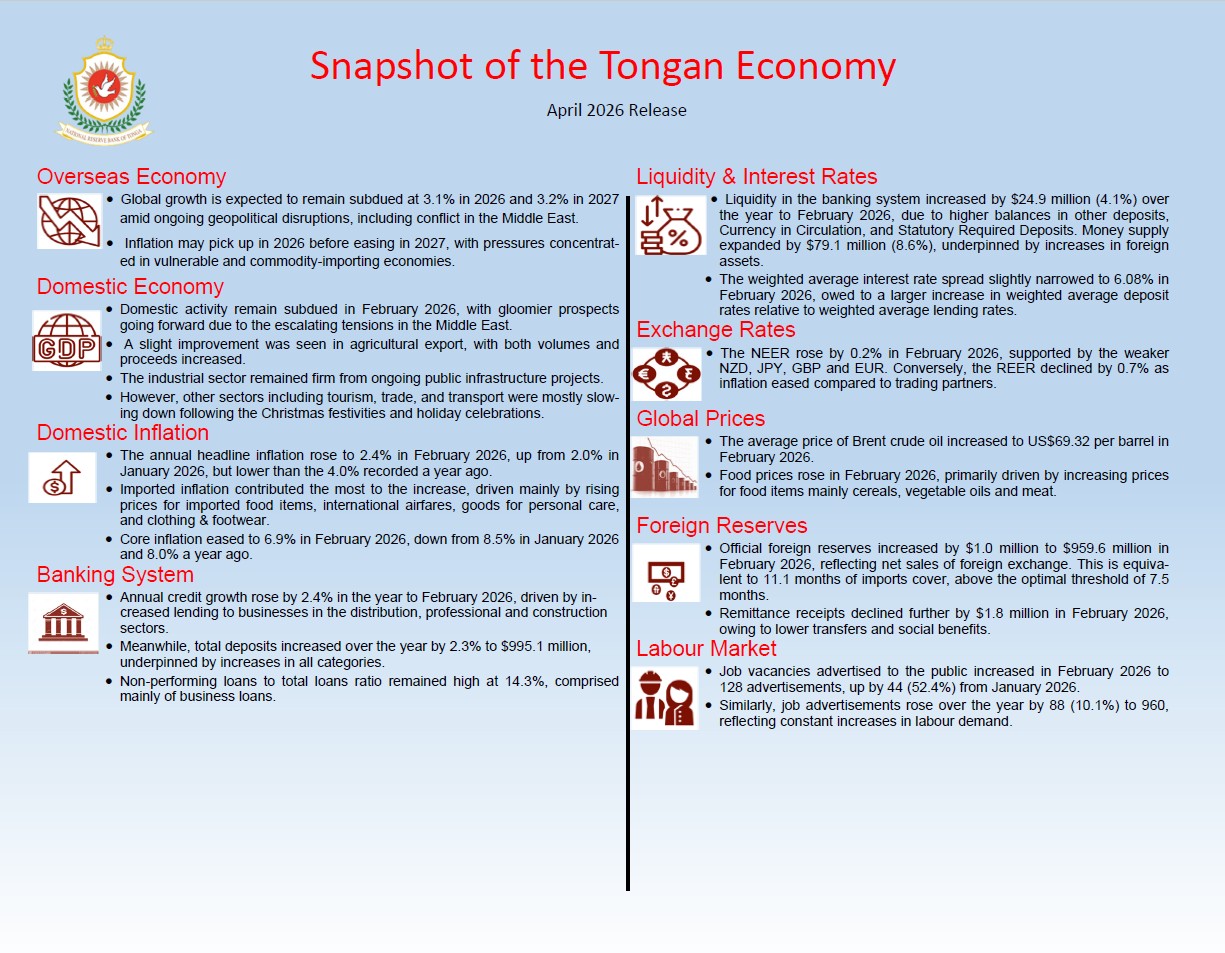

The April 2026 World Economic Outlook forecasts growth of3.1% in 2026 and 3.2% in 2027, figures that fall short of bothrecent trends and pre-pandemic averages. This softer outlook reflects continued disruptions, including the economic impact of the ongoing conflict in the Middle East. In advanced economies, growth is projected to ease to 1.8% in 2026. The United States is expected to expand by 2.3%, representing a downward revision of 0.9 percentage points (pp) from earlier forecasts. Growth in emerging markets and developing economies is also expected to slow, with output projected to rise by 3.9% in 2026. Global inflation is likely to edge up in 2026 before declining again in 2027. The main inflationary pressures are expected in emerging and developing economies, particularly in commodity-importing countries that already face structural weaknesses. The balance of risks remains firmly on the downside. Prolonged geopolitical tensions, further fragmentation of the

global economy, weaker-than-anticipated productivity gains from artificial intelligence, and renewed trade frictions could all dampen growth and destabilise markets. High public debt and limited policy space add to these concerns.

Domestic activity remained subdued

Agricultural export improved in February 2026, with volumes rising by 126.7% (403.0 tonnes) to 721.0 tonnes and proceeds increasing by 124.2% ($0.51 million) to $0.9 million, driven by higher shipments of taro, cassava, yam, and the return of

watermelon exports. Over the year to February, exports grew by 61.0% (3,562.9 tonnes) to 9,401.0 tonnes, while annual proceeds rose by 63.8% ($2.9 million) to $7.6 million, supported by stronger receipts from root crops and watermelon.

Industry sector momentum remained firm in February 2026, sustained by major infrastructure works. Continued progress on the new Parliament Building and the Fanga‘uta Lagoon Bridge sustained demand in construction, mining, and

manufacturing. Additional works, including rehabilitation of water pipelines to Vaiola Hospital and Kolomotu‘a, and energy upgrades linking the Fualu Solar Plant to the Popua Substation, further boosted activity. Tertiary sector activity continued to ease in February 2026 following the festive peak and January 2026 slowdown. Imported containers fell by 133 (13.7%) to 839, vehicle registrations edged down by 11 (3.8%) to 278, and travel activity declined sharply, with arrivals down 2,745 (26.9%) to 7,452 and departures down 4,555 (36.5%) to 7,909. Travel receipts also dropped by $6.4 million (32.3%) to $13.4 million. Despite the monthly slowdown, annual trends were more stable, with arrivals and departures slightly higher and travel

receipts rising by $26.0 million (15.3%) to $195.9 million. Import payments excluding oil fell by $10.2 million (21.9%), mainly due to weaker wholesale and retail imports, though consumer-related imports still recorded modest annual growth

of $2.8 million (0.7%), indicating some underlying resilience.

Headline inflation rose to 2.4%

Annual headline inflation rose to 2.4%, up from 2.0% in January 2026, but down from 4.0% a year earlier. Imported prices increased by 4.7%, driven mainly by higher costs for food items, international airfares, personal care goods, and clothing & footwear, while fuel and vehicle prices declined. Domestic prices rose modestly by 0.5%, reflecting higher costs for food and beverage services, alcohol, tobacco, and kava, partly offset by lower local food and electricity prices. On a monthly basis, Consumer Price Index fell by 2.3%, with both imported and domestic prices easing. Imported prices dropped 1.0%, led by declines in airfares, personal care goods, vehicles, footwear, and fuel. Domestic prices fell more sharply by 2.7%, mainly due to lower food, personal care, and tobacco costs. Core inflation (excluding food and energy) eased to 6.9%, down from 8.5% in January and 8.0% a year earlier. Domestic core items contributed about 4.7 pp, driven by food and beverage services, alcohol, tobacco, kava, and transport services. Imported core items added 2.2 pp, reflecting international airfares, personal care goods, clothing & footwear, and household furniture & equipment.

Job advertisements increased further

The NRBT’s survey recorded an increase in labour demand in February 2026, with 128 vacancies advertised, up by 44 (52.4%) from January 2026. On an annual basis, job advertisements increased by 88 (10.1%) to 960, indicating constant increases in labour demand.

Real effective exchange rate declined

In February 2026, the Nominal Effective Exchange Rate (NEER) increased marginally over the month by 0.2%, reflecting a slight strengthening of the TOP against its major trading currencies. Over the year, however, the NEER recorded a 1.7% decline, as the TOP generally weakened against most of its trading currencies. In terms of Real Effective Exchange Rate (REER) it has declined over the month and year by 0.7% and 1.3%, respectively. This reflects a gain in Tonga’s competitiveness.

Foreign reserves increased modestly

In February 2026, foreign reserves increased by 0.1% to $959.6 million, reflecting net sales of foreign exchange. This is sufficient to 11.1 months of import coverage, above the optimal threshold of 7.5 months. Over the year, the foreign reserve

increased by $80.6 million.

Remittance declined further

Remittances fell by $1.8 million in February 2026, driven mainly by a $1.9 million decrease in private transfers and a $0.07 million decline in social benefits, partially offset by a $0.2 million increase in private capital transfers, while compensation of employees remained unchanged. By currency, AUD remittances rose slightly by $0.1 million (0.4%), but this was outweighed by declines in USD remittances by $0.4 million (2.3%) and NZD remittances by $1.6 million (15.9%).

Reserve money declined while broad money increased

Reserve money (liquidity) declined by $11.5 million (1.8%) over the month of February 2026, but increased by $24.9 million (4.1%) annually. The monthly decline was driven by lower balances in the Exchange Settlement Accounts (ESA), Currency in Circulation (CIC), and Statutory Required Deposits (SRD), which outweighed gains in other deposits, including reserve bank notes. Annually, increases in other deposits, CIC, and SRD more than offset the fall in ESA, resulting in overall

growth in reserve money. Broad money rose by $4.6 million (0.5%) over the month and $79.1 million (8.6%) annually. Monthly growth was driven by an $8.7 million increase in net domestic assets, while annually, growth was supported by an $84.1 million rise in net foreign assets despite a $5.2 million decline in net domestic assets. Meanwhile, total bank deposits fell by $7.0 million (0.7%) over the month to $995.1 million, mainly due to lower demand and savings deposits.

TTotal lending remained high

After peaking in January 2026, total bank lending fell to $607.9 million, declining by 0.6% over the month but grew by 2.4% annually in February 2026. The monthly drop reflected reduced lending to both businesses and households, with declines in

sectors such as entertainment & catering, manufacturing, and professional services. In contrast, annual growth was driven by increased lending to businesses in distribution, professional services, and construction.

The Government Development Loans scheme has remained suspended since June 2024, resulting in declines of 0.6% ($0.04 million) over the month and 30.1% ($2.9 million) annually. At the same time, the loan to deposit ratio slightly rose to 60.0%, reflecting deposits declining more than the fall in loans over the month and higher deposits offsetting increase in lending annually The NPLs to total loans ratio slightly increased to 14.3%, compared with 14.0% recorded last month and 13.4% last year. This was mainly due to increases in non-performing loans to households, though business loans account for the majority of NPLs.

Interest rate spread narrowed

The interest rate spread narrowed slightly to 6.08% in February 2026, down from 6.13% in January 2026 and 6.10% a year ago. The monthly drop was driven by higher deposit rates combined with slightly lower lending rates. Over the year, the rise in deposit rates outpaced lending rates. Changes in deposit rates were led by demand and time deposits, and lending rate movements reflected shifts across key business sectors and household loans, particularly vehicle loans. The increase in deposit rates may partly reflect the issuance of NRBT notes.