- Monthly Economic Update - February 2026 DOWNLOAD THE FULL UPDATE | PDF • 605 KB

Outlook

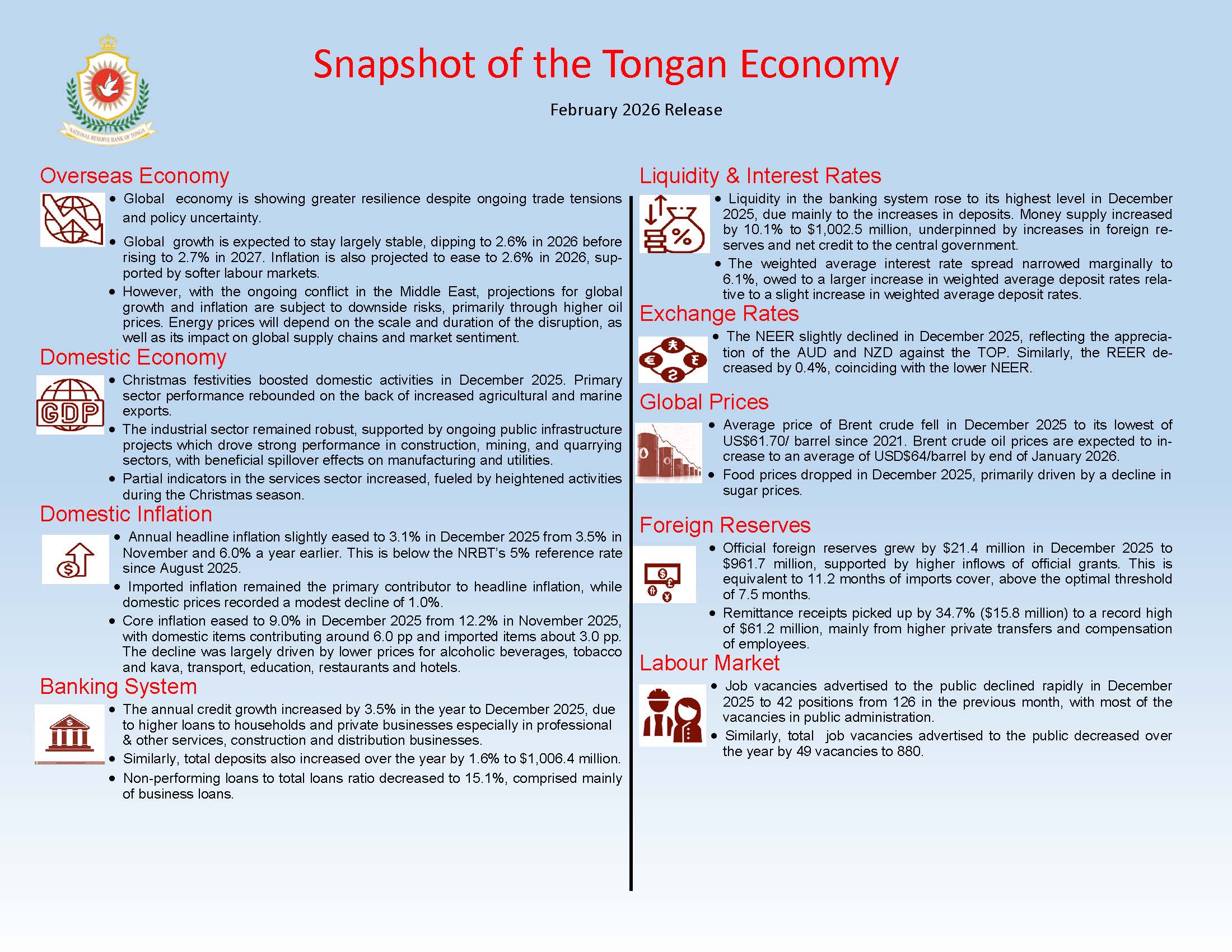

Domestic economic activity strengthened in December 2025, reinforcing the NRBT’s projections of a solid recovery in the current fiscal year. The new Government remains committed to prioritising growth, mobilising new investments and sustaining expansionary fiscal measures.

Headline inflation is currently low and core inflation eased; however, risks to the inflation outlook are tilted to the upside, with inflationary pressures expected to materialise

during the first half of 2026 and together with the escalated Middle East crisis adding a new layer of disruption, to push headline inflation above the 5% reference rate.

Foreign reserves are expected to remain above minimum thresholds in the near term, supported by steady inflows of budget support, official grants, and remittances. Meanwhile,

import payments are projected to increase alongside the economic recovery. However, the medium-term outlook remains uncertain and tilted to the downside with further

uncertainty from Middle East conflict disruptions.

The financial system remains sound, supported by high liquidity, adequate capital buffers, and sustained profitability. However, proactive oversight of vulnerabilities and risks will help to manage the impaired asset quality.

Given the current developments and outlook, the NRBT maintains its neutral monetary policy stance issued in February 2026. The NRBT modernizing monetary policy aims to strengthen transmission of the policy rate to short term market rates. This is critical to restoring monetary policy effectiveness ultimately in containing inflationary pressures and protect the public purchasing power.

Global economy shown resilience, yet outlook remains cloudy

According to the World Bank’s latest Global Economic Prospects report, the global economy is showing greater resilience than previously expected despite ongoing trade

tensions and policy uncertainty. Global growth is projected to remain broadly steady over the next two years, declining to 2.6% in 2026 before rising to 2.7% in 2027.

Inflation is also projected to ease to 2.6% in 2026, supported by softer labor markets and lower energy prices. Oil prices are projected to fall in 2026 as growth in supply is

expected to outpace demand.

However, with the ongoing conflict in the Middle East, projections for global growth and inflation are subject to downside risks, primarily through higher oil prices. Energy

prices will depend on the scale and duration of the disruption, as well as its impact on global supply chains and market sentiment.

Christmas festivities boosted domestic activities

Primary sector activities rebounded in December 2025. Agricultural exports rose by 117.9% (677.8 tonnes) to 1,252.9 tonnes, lifting proceeds by 40.1% ($0.2 million) to $0.8 million, mainly on stronger watermelon shipments despite seasonal declines in some root crops. Marine exports increased by 18.9% (51.6 metric tonnes) to 54.3 metric tonnes, driven by tuna, while aquarium exports rose by 11.1% (1,206 pieces) to 12,068 pieces. However, marine export receipts fell by 39.8% to $0.06 million, which may indicate a lag in receipts.

Positive sentiments for industry sector performance were sustained by ongoing progress in major public infrastructure projects. Construction advanced on the new Parliament

Building, while preparatory works for the Fanga’uta Lagoon Bridge and approach roads moved forward following contract finalisation. Rehabilitation of transport and energy

facilities under the National Infrastructure Investment Plan also continued, reinforcing demand for construction, mining, and quarrying services. These projects are anticipated to generate positive spillover effects across the energy and manufacturing sectors, supporting broader industry activity.

Tertiary sector activities strengthened in December 2025, supported by festive season demand. Container registrations rose sharply by 53.3% (532 units) to 1,531, driven by both business and private containers. Import payments increased by $2.2 million (3.7%) to $59.7 million, reflecting higher oil‑related imports and seasonal demand, while non‑oil imports rose by 7.2% ($3.5 million) and wholesale and retail import payments edged up 1.7% ($0.6 million). Vehicle registrations also picked up, rising by 162 units (63.0%) to 419, possibly reflecting early purchases ahead of the 10‑year import restriction on vehicles. Travel activity surged, with passenger arrivals up by 79.1% (6,526) and departures rose by 42.2% (3,950), consistent with Christmas holiday travel. Travel receipts increased by $4.1 million (29.6%) to $17.9 million.

Headline inflation slightly eased to 3.1 percent

Headline inflation eased to 3.1% in December 2025, down from 3.5% in November and 6.0% a year earlier. This is still below the NRBT’s 5% reference rate since August 2025. Imported inflation moderated to 5.5% due to smaller increases in food, clothing, and passenger transport, while domestic inflation was modest at 1.0%, driven by

restaurants, hotels, kava, tobacco, and alcohol, partly offset by lower local food prices.

Month‑on‑month, domestic prices rose by 3.5% led by local food and kava, while imported prices increased by 1.1% reflecting higher international airfares, food, and transport services. Food inflation eased over the year by 1.9%, despite a 4.8% monthly rise from both imported and domestic food items. Imported food inflation rose by 6.0% over the year, while domestic food inflation fell by 8.8%, mainly from lower prices of root crops and cereals.

Annual core inflation eased to 9.0% from 12.2% in November 2025, with domestic items contributing around 6.0 pp and imported items about 3.0 pp. The 10% trimmed‑mean core inflation edged up to 9.4% from 9.2%, indicating broad‑based underlying pressures despite the headline easing.

Job advertisements eased

Labour mobility eased in December 2025. The NRBT’s survey on job advertisements recorded a sharp decline in advertised positions by 66.1% (84 vacancies), as recruitment slowed ahead of the Christmas holidays. On an annual basis, job advertisements fell modestly by 5.3% (49 vacancies) to 880, indicating a slight softening in labour demand compared to the year ending December 2024.

Real exchange rates strengthened

The Nominal Effective Exchange Rate (NEER) fell by 0.3% in December 2025, reflecting the appreciation of the AUD, NZD and FJD against the TOP. Over the year, the NEER recorded a 1.3% decline, driven by the weakening of the TOP against the AUD and NZD. The Real Effective Exchange Rate increased by 2.0% during the month but declined by 0.4% over the year.

Foreign reserves increased further

In December 2025, foreign reserves increased by 2.3% ($21.4 million) to $961.7 million, supported by higher inflows of official grants. This is equivalent to 11.2 months of import coverage, above the optimal threshold of 7.5 months. Over the year, foreign reserve increased by $72.7 million.

Remittance receipts climbed to a record high

Remittance receipts rose sharply by 34.7% ($15.8 million) in December 2025 to a record of $61.2 million. The majority of remittances were private transfers from family and friends abroad (88%), followed by compensation of temporary workers abroad (10%). AUD dominated receipts at nearly 40%, followed by USD at 35% and NZD at 20%.

Liquidity peaked

Reserve Money rose by 1.6% ($10.0 million) over the month and by 3.3% ($21.0 million) over the year, climbing to $656.6 million, its highest level on record. The monthly increase was driven solely by higher balances in Banks’ Exchange Settlement Accounts (ESA), which offset declines in Currency in Circulation (CIC), Statutory Reserve Deposits (SRD) and other deposits. On an annual basis, however, CIC, SRD, and other deposits all recorded gains which offset the lower ESA.

Broad money increased by 3.1% ($31.2 million) over the month and by 10.1% ($91.7 million) over the year, setting a new all-time high of $1,002.5 million. The monthly and annual expansions in liquidity were mainly due to higher net foreign assets, with additional support from net domestic assets over the year. The rise in foreign assets came from

increased foreign reserves and other external holdings. Growth in domestic assets was driven by more lending to the government and higher capital accounts. Meanwhile, total bank deposits expanded by 1.8% ($17.8 million) to $1,018.2 million, supported by robust demand and savings deposits.

Credit growth slows on weaker business lending

Total bank credit eased in December 2025, slipping by $1.4 million (0.2%) to $610.4 million, reflecting weaker business lending, which offset November’s strong expansion. Despite the monthly slowdown, annual growth remained firm, rising by $20.6 million (3.5%), underscoring resilience in overall credit activity.

Over the month, business lending contracted by $2.7 million (0.8%), led by reduced borrowing from public enterprises and private firms in distribution, transport, and manufacturing. In contrast, household credit rose by $1.4 million (0.8%), driven by other personal loans.

Annually, lending to both households and businesses increased by 4.1% ($11.5 million) and 2.9% ($9.0 million), respectively. The rise in households lending reflected stronger housing loans, complemented by gains in other personal and vehicle loans. Similarly, business lending was buoyed by higher credit to private firms, especially in professional & other services and construction.

Government Development Loans portfolio continued to contract, both monthly and annually, reflecting the ongoing suspension of the scheme. Meanwhile, the loan to deposit

ratio climbed to 59.6%, as falling deposits signaled tighter funding conditions.

The non-performing loans (NPL) to total loans ratio improved over the month and year, declining from 15.1% and 14.6% to 14.4%, with most NPL’s concentrated in business loans.

Interest rate spread widened

The weighted average interest rate edged up over the month by 3.6 bps to 6.1%, driven by a 2.7 bps increase in weighted average lending rate alongside a 0.9 bps decline in weighted average deposit rate.

Annually, however, the weighted average interest rate spread narrowed marginally by 0.7 bps, due mainly to a larger increase in weighted average deposit rates (6.8 bps) relative to the rise in weighted average deposit rates (6.1 bps).