- Monthly Economic Update - March 2026 DOWNLOAD THE FULL UPDATE | PDF • 605 KB

Outlook

Amidst the ongoing geopolitical conflict in the Middle East and heightened global uncertainties, domestic economic activity is expected to be constrained by disruptions in international markets and trading dynamics with major partners. These developments are anticipated to exert a more immediate impact on Tonga’s economic activities than previously expected, reflecting elevated market risks and volatility.

The outlook for inflation remains highly contingent on the trajectory of the conflict and its associated uncertainties. Current developments in global oil markets point to a pronounced and sustained upward trend, intensifying pressures on core goods and services. The challenge is compounded by the limited capacity of domestic production to absorb external shocks, heightening the risk of pass-through effects and prolonged inflationary pressures.

Foreign reserves are expected to remain above minimum thresholds in the near term, supported by steady inflows from budget support, official grants, and remittances. However, the medium-term outlook remains uncertain and is tilted to the downside, particularly if the ongoing Middle East crisis persists.

Meanwhile, the financial system remains sound, supported by high liquidity, adequate capital buffers, and sustained profitability. However, the elevated level of non-performing loans (NPLs) underscores the need for prudent lending practices and enhanced oversight. NPLs are expected to increase further if the impact of the Middle East crisis intensifies, as businesses and households may face greater difficulty servicing their loans, leading to higher default rates.

In light of these developments and the outlook, the NRBT and the Government are working closely together to mitigate risks arising from the crisis, particularly the risk of stagflation. Meanwhile, NRBT notes will continue to be utilised to absorb the excess liquidity in the banking system and to strengthen the effective transmission of monetary policy to market interest rates. Efforts to enhance liquidity management, reactivate the interbank market, modernise payment systems, and deepen financial markets are ongoing.

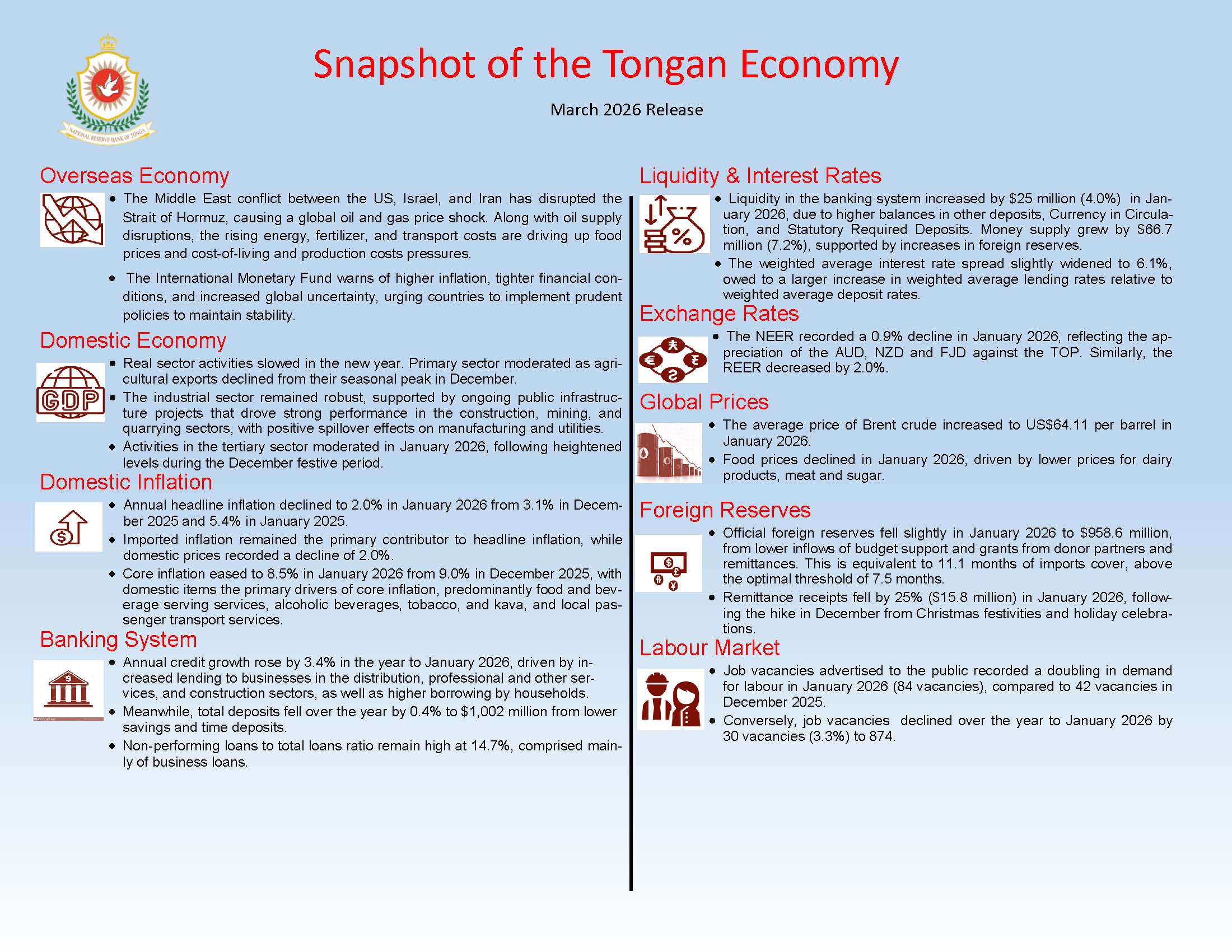

The Middle East war to have significant impact on global economy

The Middle East conflict between the US-Israel and Iran that escalated on February 28th has disrupted shipping through the Strait of Hormuz, the world's most critical oil chokepoint. This has led to a substantial global oil and gas price shock. The ongoing military escalation is generating ripple effects that extend far beyond the region impacting energy markets, maritime transport, and global supply chains.

As a result, Brent crude oil prices have surged toward $120 per barrel. Rising energy, fertilizer, and transport costs including freight rates, bunker fuel prices, and insurance premiums are likely to increase food prices and intensify cost-of-living pressures, particularly for the most vulnerable populations, and production costs.

The International Monetary Fund (IMF) warns that the Middle East war will lead to higher prices, tighter financial conditions, and greater global economic uncertainty. IMF is closely monitoring the situation and supporting vulnerable countries with policy advice and financial assistance. To cope with the shock, countries must respond carefully with appropriate policies to remain stable and avoid deeper economic problems.

Domestic economic activities slowed in the new year

In January 2026, primary sector activity moderated as agricultural exports dropped sharply by 74.6% to 318.0 tonnes, reflecting the seasonal peak of watermelon shipments in the previous month and reduced volumes of root crops such as cassava, taro, and yam. Export proceeds also fell by 51.0% to $0.4 million. However, over the year to January 2026, exports volume rose by 52.4% (3,099.3 tonnes) to 9011.8 tonnes supported by stronger shipments of root crops and watermelon, with annual proceeds increasing by 65.4% to $7.8 million.

Industry sector momentum is sustained by major infrastructure works, including the new Parliament Building and the landmark Fanga’uta Lagoon Bridge, one of the largest transport projects in Tonga. Alongside rehabilitation of energy and transport facilities under Tonga National Infrastructure Investment Plan (NIIP), these initiatives are reinforcing demand for construction, mining, and manufacturing, while delivering climate resilience and broader economic spillovers.

Tertiary sector activities eased in January 2026, following December’s festive peak. Imported containers fell by 559 (36.5%), with declines in both business and private shipments, reflecting a post-Christmas slowdown after higher festive import activity. Vehicle registrations fell by 130 units (31.0%) to 289, with annual registrations down slightly by 122 (3.5%) to 3,380. Travel activity declined, with both arrivals and departures falling. However, travel receipts rose due to higher tourist spending. Over the year, arrivals were slightly lower and departures higher, while travel receipts increased strongly, indicating resilient tourism inflows.

Headline inflation dropped to 2.0%

The annual headline inflation further declined to 2.0% in January 2026, from 3.1% in December 2025 and 5.4% in January 2025. Imported inflation edged up to 6.0% driven by imported food items, passenger transport services (international airfares), goods for personal care, and clothing and footwear. In contrast, domestic prices fell by 2.0% compared to January 2025, largely due to lower prices of local food items.

On a monthly basis, the Consumer Price Index declined by 0.6% in January 2026, due to overall decreases in both imported and domestic prices. Imported prices fell by 1.8% over the month, due to lower cost of passenger transport services (international airfares), and goods for personal care. Meanwhile, domestic prices decreased by 0.3% largely owed to lower price of local food items, and cost of electricity. Local food prices recorded a 6.0% decline over the month which may indicate a slowdown to the heightened demand of the Christmas season.

Annual core inflation (excluding food and energy) eased to 8.5% in January 2026, a decline from 9.0% in December 2025. Domestic items were the primary drivers of core inflation, particularly food and beverage serving services, alcoholic beverages, tobacco, and kava, and local passenger transport services. Imported components also contributed, most notably passenger transport services (international airfares), goods for personal care, and clothing and footwear.

Job advertisements strengthened

The NRBT’s survey on job advertisements recorded a 100.0% increase by 42 to 84 vacancies compared to the 42 advertised vacancies in December 2025, reflecting stronger demand for labour following the holiday period. On an annual basis, job advertisements fell modestly by 3.3% (30 vacancies) to 874, indicating a slight softening in labour demand compared to January 2025.

Effective exchange rate declined

The Nominal Effective Exchange Rate (NEER) fell by 0.9% in January 2026 due to the appreciation of the AUD, NZD, and FJD against the TOP. Over the year, it declined by 2.0%, mainly from a weaker TOP against the AUD and NZD. The Real Effective Exchange Rate also dropped by 2.0% over the month and 1.7% annually.

Foreign reserves eased

In January 2026, foreign reserves decreased by 0.3% to $958.6 million due to lower inflows of budget support and grants from donor partners and remittances. This is equivalent to 11.1 months of import coverage, above the optimal threshold of 7.5 months. Over the year, foreign reserve increased by $80.6 million.

Remittance receipts fell

Remittances fell by 25.8% ($15.8 million) in January 2026 following a hike in the previous month, mainly due to lower private transfers and worker compensation. Most receipts came from family and friends abroad (88%), with temporary workers contributing 10%. The AUD was the main currency, followed by USD and NZD. The NRBT estimates that remittances represent around 40% of GDP, underscoring their importance to Tonga’s economy and household welfare.

Money supply increased whilst reserve money declined

Reserve money, or liquidity, fell over the month of January 2026 by $6.1 million (0.9%), however increased annually by $25.0 million (4.0%). The monthly decline was due to lower balances in the Exchange Settlement Accounts (ESA), Currency in Circulation (CIC), and Statutory Required Deposits (SRD), which outweighed the increase in other deposits, mainly NRBT notes. Annually, growth in other deposits, CIC, and SRD more than offset the fall in ESA, leading to an overall rise in reserve money.

Broad money increased both monthly (1.9%) and annually (7.2%). Monthly growth was driven by higher net domestic assets from stronger private sector credit, while annual growth stemmed from rising net foreign assets. Meanwhile, total bank deposits declined slightly (0.4%), due to lower savings and time deposits.

Total lending peaked

Banks’ total lending reached a record high of $611.9 million, rising slightly over the month (0.2%) and more strongly over the year (3.4%), mainly due to increased business lending. Business loans grew, driven by public enterprises and private firms, while household lending fell slightly as declines in housing and personal loans outweighed growth in vehicle loans. Over the year, both business and household lending increased, supported by gains across several sectors.

The Government Development Loans scheme has been suspended since June 2024, leading to declines both monthly and annually. Meanwhile, the loan-to-deposit ratio rose to 60.2% as lending growth outpaced falling deposits.

The NPLs to total loans ratio remain high 14.7%, with business loans making up the largest share of NPLs.

Interest rate spread widened

The interest rate spread rose to 6.1% in January 2026, increasing slightly over the month and year. The monthly rise was due to lower deposit rates outweighing a small drop in lending rates. Deposit rates declined mainly for businesses, while lending rates fell across several sectors, including households due to lower personal loan rates.

Over the year, lending rates increased more than deposit rates, widening the spread. Higher lending rates were driven by financial corporations and key business sectors, along with rising household loan rates. Deposit rates also grew overall, supported by higher placements from government, retirement funds, and the private sector.