- Monthly Economic Update - May 2026 DOWNLOAD THE FULL UPDATE | PDF • 605 KB

Outlook

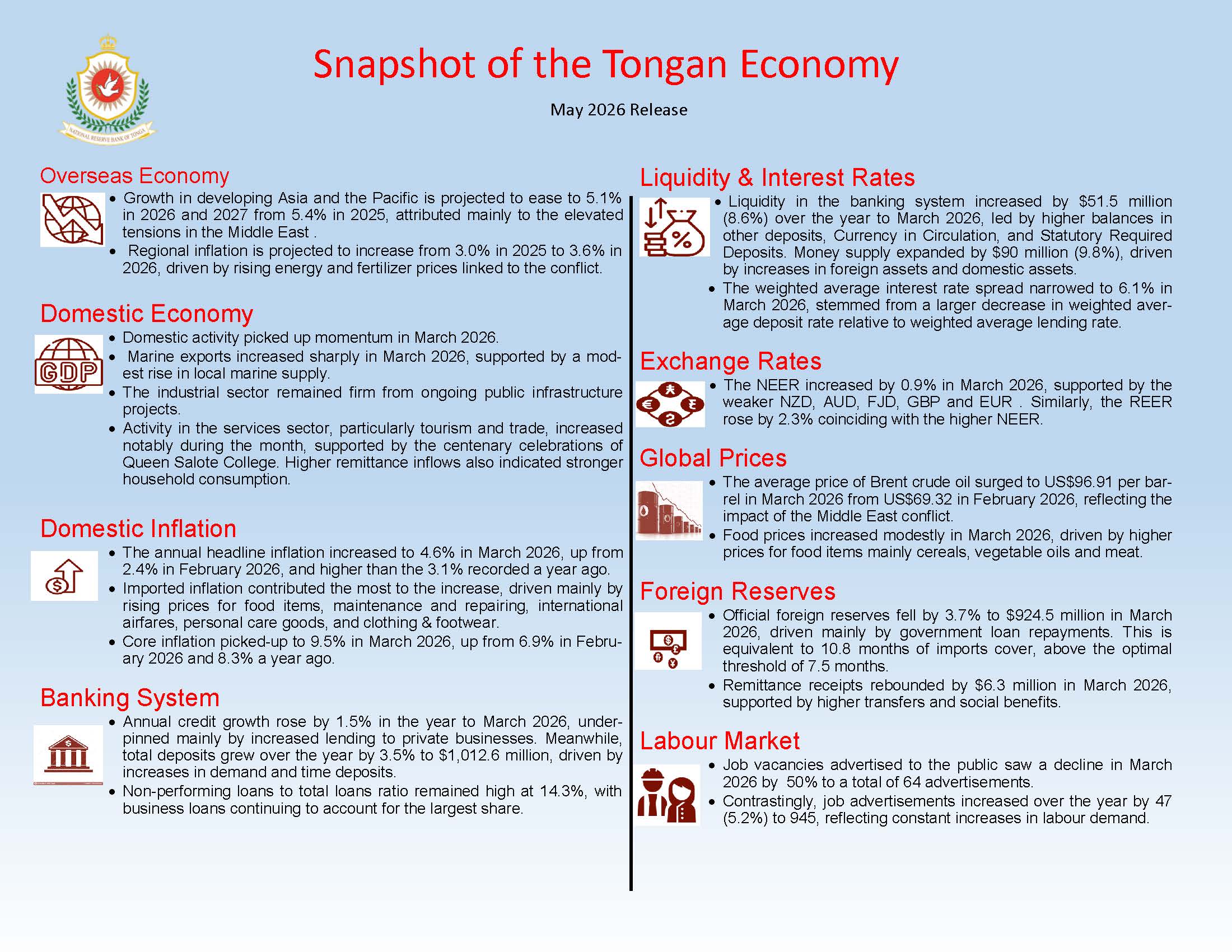

The outlook for Tonga's economy remains subject to significant external risks given the ongoing Middle East conflict and heightened global uncertainty. The conflict has pushed up global energy prices, which are expected to increase fuel, freight, and import costs in the coming months. Authorities continue to closely monitor developments to ensure adequate fuel supplies are maintained in the face of potential global oil supply disruptions.

Inflation is projected to remain above the NRBT’s reference rate in the near term, largely depending on the duration and intensity of the conflict. Higher global oil and shipping costs are expected to continue exerting upward pressure on domestic prices, particularly for fuel, transport, food, and other imported goods.

Official foreign reserves are expected to remain adequate, supported by external inflows. However, risks to the external sector have increased, particularly if higher import costs persist or global economic conditions weaken further.

The financial system remains resilient, maintained by strong capital buffers and ample liquidity. Nevertheless, credit growth may remain subdued as economic uncertainty weighs on business investment and household borrowing. Asset quality may face further pressures if elevated fuel prices and living costs persist, placing additional strain on household incomes and business cash flows.

In response to these challenges, the NRBT and Government will continue to coordinate closely to mitigate inflationary risks and safeguard macroeconomic stability. Ongoing efforts will focus on strengthening liquidity management, enhancing payment systems, and deepening financial markets to support financial stability and economic resilience.

Global risks and inflationary pressures continue to weigh on the outlook

The Asian Development Bank's April 2026 outlook projects growth in developing Asia and the Pacific to ease to 5.1% in 2026 and 2027 from 5.4% in 2025, mainly due to the economic effects of the Middle East conflict. Higher energy costs are expected to raise production expenses and consumer prices, while export growth moderates following earlier front-loading ahead of U.S. tariff increases. However, strong domestic demand is expected to continue supporting regional growth.

Regional inflation is forecasted to increase from 3.0% in 2025 to 3.6% in 2026, driven by rising energy and fertilizer prices linked to the conflict.

Meanwhile, the Reserve Bank of Australia raised its cash rate to 4.35% in May 2026, reflecting persistent inflationary pressures. In contrast, the Reserve Bank of New Zealand kept its Official Cash Rate at 2.25% in May 2026 in response to the current economic conditions, including soft domestic demand, subdued business investment and weakened labour market conditions.

Domestic activity regained momentum

In March 2026, agricultural exports fell by 57.9 tonnes (8.0%) to 663.2 tonnes, and proceeds declined by $0.18 million (19.4%) to $0.7 million. This was due to lower exports of taro and sweet potatoes, despite increases in cassava, yam and kava exports. However, agricultural exports rose over the year by 2,698.3 tonnes (42.1%) to 9,106.9 tonnes, with proceeds increasing by $3.4 million (66.2%) to $8.5 million. Marine exports rebounded sharply in March 2026 to 129.2 tonnes compared to 6 tonnes in February 2026, driven by a significant increase in tuna shipments by 122.8 tonnes.

Activities in the industrial sector remained robust in March 2026, supported by ongoing major infrastructure projects including the new Parliament Building and the Fanga‘uta Lagoon Bridge, which continued to drive construction, mining, and manufacturing activities. Further momentum was provided by new contracts for the Nuku‘alofa Parliament compound and road safety upgrades. Progress under the Tonga Infrastructure Pipeline Workshop and Green Climate Fund training also strengthened long-term infrastructure planning and climate financing for future industrial growth.

In March 2026, services sector activity rebounded following February’s slowdown. Container registrations grew by 212 (25.3%) to 1,051 containers, driven by increases in both business containers and private containers. This coincided with a rise in import payments excluding oil of $7.0 million (19.2%), supported by higher wholesale and retail imports. Vehicle registrations declined by 18 (6.5%) over the month to 260 registrations, predominantly due to fewer registrations of light and heavy vehicles. Meanwhile, tourism-related activities picked up during the month, with visitor arrivals increasing by 2,670 (30.3%) to 11,490, departures rising by 2,612 (30.0%) to 11,321, and travel receipts growing by $1.5 million (11.1%) to $14.9 million. The increase was largely driven by influx of overseas visitors attending the week-long centenary celebrations of Queen Salote College, particularly ex-students returning from abroad.

On an annual basis, container registrations fell by 937 (7.3%) to 11,829 containers, underpinned by a 971 (8.8%) decline in business containers. Contrastingly, total vehicle registrations increased by 43 (1.2%) to 3,505, driven by a strong growth in car registrations (37.0%) and motorcycles (47.1%). Tourism activity also remained positive, with visitor arrivals increasing by 1,090 (0.9%) to 126,122 and departures rising by 9,651 (8.3%) to 125,441. Travel receipts also picked up by $29.5 million (17.3%) to $200 million.

Headline inflation rose to 4.6%

Annual headline inflation increased to 4.6% in March 2026, up from 2.4% in February 2026 and higher than the 3.1% a year ago. Imported prices increased by 6.9%, driven mainly by higher prices for food items, maintenance and repairing, international airfares, personal care goods, and clothing & footwear. Domestic prices rose by 2.5%, reflecting higher prices for food and beverage services, alcohol, tobacco, kava, transport, and education.

On a monthly basis, the Consumer Price Index rose by 1.5%, with both imported and domestic prices increasing. Imported prices increased by 2.3%, led by transportation, while domestic prices increased by 0.8%, mainly due to food, alcohol, tobacco, and kava.

Core inflation (excluding food and energy) accelerated to 9.5% in March 2026, up from 6.9% in February 2026 and 8.3% a year earlier. Domestic core items contributed 4.4 percentage points (pp), driven by food and beverage services, alcohol, tobacco, kava, and passenger transport services, while imported core items added 5.2 pp, reflecting higher costs for personal care goods, clothing & footwear, and household furniture & equipment

Job advertisements declined

The NRBT’s survey recorded a sharp decline in labour demand by 64 (50%) vacancies in March 2026. These vacancies were mostly in public administration, transport & communication, and real estate & business services. On an annual basis, vacancies rose by 62 (6.9%) to 945, reflecting constant increases in labour demand for public administration and, transport & communication.

Effective exchange rate rose further in March 2026

The Nominal Effective Exchange Rate (NEER) increased by 0.9% in March 2026, reflecting the appreciation of the TOP against the NZD, AUD, FJD, GBP and EUR. Over the year, the NEER recorded a 0.5% decline, as the TOP depreciated against all the trading currencies except for the USD and NZD. The Real Effective Exchange Rate on the other hand, increased over the month and year by 2.3% and 1.2%, respectively.

Foreign reserves declined

Official foreign reserves decreased by 3.7% to $924.5 million, underpinned mainly by government loan repayments. Despite the decline, reserves remained sufficient to cover 10.8 months of imports, above the optimal threshold of 7.5 months. Over the year, foreign reserve increased by $81.9 million.

Remittances rebounded

Remittances rose by $6.3 million in March 2026, driven mainly by increases in private transfers and compensation of employees by $5.2 million and $1.3 million, respectively. By currency, remittances inflows were led by the NZD which increased by $2.1 million (25.4%), followed by the AUD by $2.1 million (11.4%), and the USD by $1.7 million (11.4%).

Reserve money and broad money increased

Reserve Money (liquidity) rose over the month and year in March 2026, rising by $11.8 million (1.8%) and $51.5 million (8.6%), respectively. The monthly increase was attributed to higher balances in other deposits, including NRBT notes and Currency in Circulation (CIC), which outweighed declines in Exchange Settlement Accounts (ESA) and Statutory Required Deposits (SRD). Annually, growth in other deposits, CIC, and SRD more than offset the fall in ESA, resulting in a net rise in reserve money.

Broad money expanded by $10.3 million (1.0%) over the month and by $90.0 million (9.8%) annually in March 2026. The monthly growth was driven by a $41.1 million increase in net domestic assets, which more than offset a $30.7 million (3.2%) decline in net foreign assets. Over the year, both net foreign assets and net domestic assets contributed to growth, rising by $78.8 million (9.3%) and $10.9 million (15.9%), respectively. Meanwhile, total bank deposits climbed by $17.5 million (1.8%) over the month to $1,012.6 million, mainly due to higher demand and savings deposits.

Total lending grew in March 2026

Total lending including GDL grew over the month and year to March 2026 by $2.6 million (0.4%) and $8.9 million (1.5%), respectively. Monthly growth was driven by lending to public enterprises and private businesses, particularly in distribution, manufacturing, and construction, while annual growth reflected increased lending to private businesses in distribution, construction, and entertainment and catering.

Government Development Loans (GDL) resumed after being suspended since June 2024; however, balances declined by 0.2% ($0.01 million) over the month and 29.6% ($3.4 million) annually, as repayments outweighed new loan disbursements. At the same time, the loan to deposit ratio fell to 59.2%, reflecting deposit growth outpacing the rise in loans both over the month and annually.

The Non-Performing Loan (NPL) ratio remained unchanged at 14.3% from the previous month but increased from 13.1% a year ago, largely due to higher business loan defaults, which continue to account for the majority of NPLs.

Interest rate spread widened

The weighted average interest rate spread widened slightly by 0.2 basis points to 6.1% in March 2026, as deposit rates declined more than lending rates over the month. However, the spread narrowed by 1.4 basis points compared to a year earlier, reflecting a larger increase in deposit rates than in lending rates over the year.